Inflation

Fed Chair Warsh's debut signals hawkish shift: no forward guidance, focus on price stability, institutional reform. Markets price in rate hikes. Full analysis.

Fed Chair transition May 22, 2026: Powell's final decision, Warsh's hawkish monetary policy changes. Iran war complicates Fed handoff. Market analysis.

Market outlook 2026: Geopolitical tensions drive oil prices, AI infrastructure spending concerns, private credit risks. Analysis of Q1 performance and outlook.

Foreign investors poured $1.55 trillion into US assets in 2025—not selling America, but rotating from bonds to stocks. Discover why global diversification is now essential for investors.

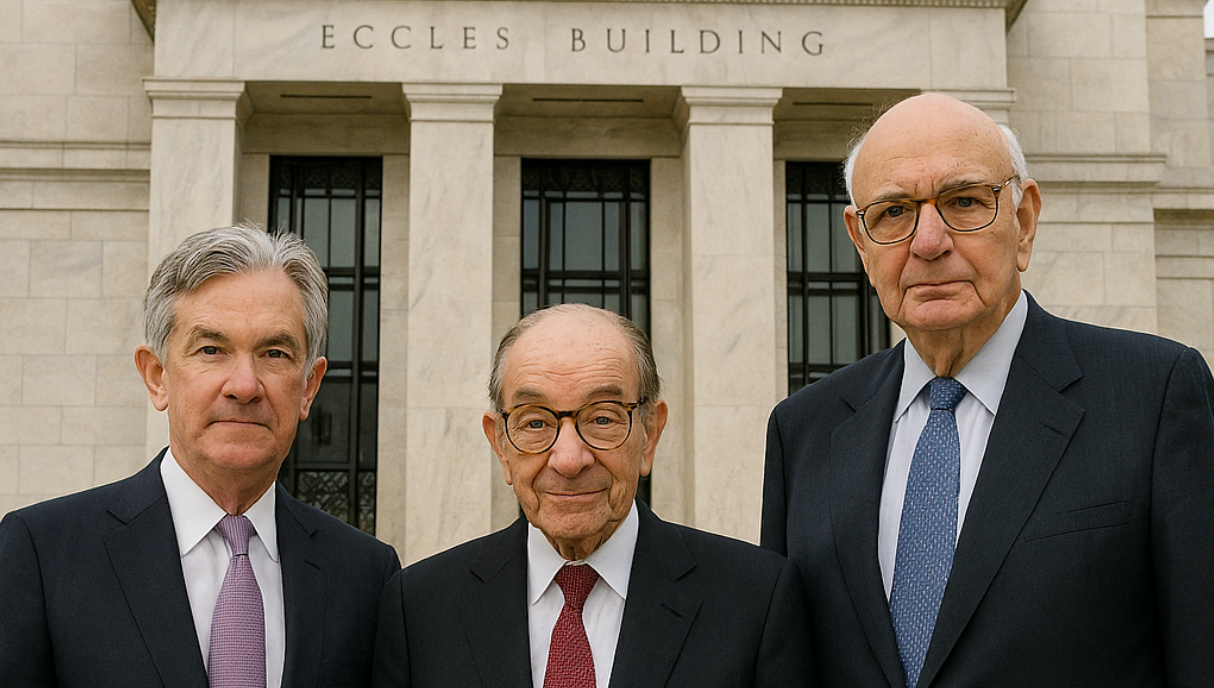

Learn about the US Federal Reserve System's structure, history, and current leadership. Understand the Fed's dual mandate, FOMC meetings, and how Fed policy decisions impact investors and consumers.

We have all heard the adage… “Don’t fight the Fed.” That was sage advice back in 2022 as the Fed embarked on the most aggressive tightening cycle dating back 40 years. That year both stocks and bonds withered, ending the year down by double digits, you would have to go back to 1941 the last time both asset classes showed losses for the year when you use the 10-year Treasury as a proxy for the bond market. Now with the pendulum shifting from tightening monetary policy to “easier money” everyone is trying to understand what that means for the economy and their portfolio in the months and years ahead. Lately the narrative has shifted a bit, there is a growing chorus that believes that monetary policy and by that we are really referring to the Fed’s setting of overnight interest rates in an economy dominated by bits and bites versus the more tangible attributes of yesteryear has less impact today. Or perhaps, it’s those long and variable lags Milton Friedman was referring to as higher rates are still making their way through the economy. If that is the case it stands to reason that even if liftoff is September it may take time for lower rates to exert their influence. In this piece we are going to explore rates from a few different perspectives. One thing to make clear, we are not market timers and market rates are a byproduct of not just Fed policy, but numerous other factors, like growth and inflation expectations, fiscal policy, the state of geopolitics etc… We can use the past as a prologue have been taking and will continue to take some steps on behalf of our clients whose assets we are managing for important life goals. Equity Investing U.S. Stocks When the Federal Reserve cuts interest rates, it typically has a positive impact on US stock markets. If that is to play out again now, making sure that your portfolio is allocated properly when the Fed is inclined to cut rates is critically important. Here are some key points on how and why this occurs: Lower Borrowing Costs : Reduced interest rates make borrowing cheaper for companies and consumers. Newly lowered rates can lead to increased spending and investment, which often boosts corporate profits and, consequently, stock prices. Increased Consumer Spending : With lower interest rates, consumers may be more prone to take out loans for big-ticket items like houses and cars. Increased consumer spending can drive higher sales and earnings for companies, positively affecting their stock prices. Improved Corporate Earnings : Companies with existing debt benefit from lower interest payments, which can improve their profitability. This can lead to higher stock valuations. Shift from Bonds to Stocks : Lower interest rates typically lead to lower yields on bonds. Investors seeking higher returns might move their investments from bonds to stocks, positively impacting stock prices. Economic Confidence : A rate cut is often seen as a proactive move by the Fed in support of the economy. This can boost investor confidence, leading to increased buying activity in the stock market. Sector-Specific Impacts : Certain sectors, such as technology and consumer discretionary, often benefit more from lower interest rates due to their reliance on borrowing for growth and consumer spending patterns. Sectors that are highly capital intensive or with significant fixed costs stand to benefit more than asset light business historically. Financials tend to see their net interest margins or “NIM” shrink as rates come down, though a protracted period with an inverted yield curve may be less make lower rates less of a headwind if the curve returns to its normal sloping relationship where longer rates are higher than shorter rates. Manufacturers could see a benefit if lower rates mean a lower dollar making their goods more competitive when it comes to global trade. Small Cap Stocks With the incredible rise of the Magnificent 7 stocks, small cap stocks have been overlooked. A change in outlook by the Fed may create an environment for small cap stocks to continue to climb. Lower Borrowing Costs : Small-cap companies, which often have higher debt ratios than larger companies, benefit considerably from reduced interest expenses when rates are cut. Lower borrowing costs can improve their profitability and support expansion efforts whether it be adding to their workforce or expanding research & development. Growth Potential : Small-cap stocks are typically seen as growth-oriented investments. Afterall, companies that are now among the largest companies in the world like Amazon, Apple, Nvidia and Microsoft all started as small caps! Lower interest rates can spur economic activity, benefiting smaller companies that may be more agile and able to capitalize on new opportunities. Increased Risk Appetite : Rate cuts can increase investor confidence and risk appetite. Investors may be more willing to invest in higher-risk, higher-reward small-cap stocks during periods of lower interest rates. Access to Capital : Lower interest rates can make it easier and cheaper for small companies to raise capital, whether through loans or equity offerings. This can help them invest in growth initiatives, leading to higher stock prices. Overseas Equities Yield differentials may narrow : Foreign capital has been lured into US assets for many years dating back to the European Debt Crisis in the early 2010s. If US interest rates look less attractive by comparison than foreign capital may be onshored and find its way into local stock markets. A weaker dollar may ease inflation and lower borrowing costs : A more common phenomenon in the emerging markets where consumption of commodities represent larger percentages of overall spending may allow for capital to be directed more productively and as foreign companies and countries often offer dollar bonds to institutional investors to hedge the currency risk the cost of that interest could drop if the local currency strengthens vs. the dollar. Foreign assets may offer a store of value : Should the dollar weaken, it stands to reason that it’s losing ground to some other currency; that relationship can serve as a hedge to offset the diminishing purchasing power of local assets. After a long run with a stronger dollar, if there is a secular shift underway that will unfold over the years ahead, having some additional exposure aboard would be valuable from both a risk and return perspective. The combination of more attractive valuations should provide a little extra incentive to increase the ex-US holdings in the portfolio, even if it is just at the margins. One thing to keep in mind, in the past monetary policy has generally been pretty well coordinated, but if that is to change in the years ahead it will be that much more important to have some professional oversight to help navigate what could result in a little more short-term volatility. Stocks historically have fared well when the easing cycle begins, though it’s not always the case, especially if the easing is in response to a shock to the economy or deteriorating fundamentals. The latter does not appear to be the case today though there are signs of continued cooling in the labor markets where with the former, a shock, well, that’s tough to predict, after all it wouldn’t be considered a shock. It’s those known unknowns or unknown unknowns, that get you in trouble to quote the late Donald Rumsfeld.

Japan is back… Where were you in 1989? It is a welcome sight witnessing the Japanese stock market get back to levels it last touched when I was wearing tube socks and playing Nintendo. In the first quarter the TOPIX was up 10.05% matching the S&P 500 torrid start to the year. But it’s not just in the capital markets that are buzzing. You could stay up late watching Bloomberg Asia during market hours but since that should be time to wind down, you won’t be disappointed taking in two of the best series on television right now… Max’s Tokyo Vice and Shogun on FX. The world’s third largest economy as measured by GDP deserves some love. Between pop culture and higher stock prices it’s a new dawn in The Land of the Rising Sun.We are in the midst of March Madness, the pinnacle of excitement in “amateur sports” it’s hard to replicate something so immersive and exciting, but I worry the combination of the NIL and sports betting has irreparably damaged the purity of the tournament. We are all aware by now that the pandemic ushered in new era of gamification and gambling providing a much-needed distraction and some excitement in those dark days of lockdowns and masks. When it comes to wagering it’s common knowledge the house always wins. All you need to do is look at the gambling stocks which have been on a tear as they quietly pick your pockets. I have my thoughts about legalizing drugs and making gambling more accessible, but rather than pontificate, I have a more compelling suggestion. On any given day, the stock market chances for an increase is no greater than a coin toss. Alas if you buy a stock or fund you get to play that same wager over 240 times a year and rather than the “house” ending up ahead in the long run you likely have a lot more to show for it.The death of Nobel prizing winning psychologist Danny Kahneman last month had me reflecting on a true intellectual giant’s contributions to the world of behavioral finance and its value to the everyday investor. Even for someone who has spent more than two decades honing my craft, I am often surprised/amused at the tricks our minds play on us when it comes to investing. Dr. Kahneman’s seminal work Thinking, Fast & Slow is a true masterpiece, but many struggle to make their way through it. Michael Lewis’s 2016 Undoing Project is a wonderful tribute to Danny and his best friend Amos Tversky, and is a really approachable read for those unwilling to commit to the intellectual density of T, F & S. Any investor would be well served to learn about loss aversion recency bias or the endowment effect to name just a few of those blasted biases. Just when you thought people were coming to their senses and the crypto bust of 2021-2022 rid us of the daily digital data dump, here we are again with the biggest grift in modern times. I have to give it to them, despite lacking a compelling use case the Bitcoin believers have talked their way into one of the most epic executions of the greater fool theory in the history of man. Happy to have Wall Street get in on the rouse, the SEC and the sponsors of the various Bitcoin ETFs should be ashamed of themselves. Making it easier for people to lose their hard earned money is not why we are in this business and anything to “legitimize” an endeavor that has funded terrorism, human trafficking and the drug trade all for some basis points is an embarrassment. While we are on the topic of dereliction of duty, has anyone spoken with a family trying to navigate the FAFSA process this year? It’s bad enough that it costs $90,000 for a year at a prestigious liberal arts college, but to think we are making it more difficult to apply for and receive aid. You wonder why the younger generations are fed up and both sentiment levels and the government’s approval rating is at historically low levels despite a stock market at all-time highs and an unemployment rate under 4%. Applications for aid are down 57%, you read that right while the costs of college skyrocket. And those that applied were working with incomplete data. I can’t make this stuff up. We are supposed to be taking care of those in need, but we are more likely to see students take on more debt. If there was ever a better reason to start plowing money into the 529 plans now then let me know. It’s not to say we shouldn’t take the aid available to us, but perhaps it’s best to be in a position where we don’t need to count on it. George Carlin may have been thinking about another dirty word when he heard someone mutter the word inflation. It’s surely making the current administration cringe with the election less than 7 months away. While the rate of price changes have dropped markedly from their peaks in the summer of 2022, recent data suggests the victory lap for Fed which kicked off in October coinciding with this strong rally, may have been a bit premature. Coming into the year the market was pricing in 6 or even 7 rate cuts but a combination of better labor data and price stickiness has reduced the probability of aggressive easing getting under way. Just this week, on Monday, the ISM Manufacturing Survey showed we entered expansion territory in March for the first time since the Fall of 2022 and now the odds suggest just two cuts may be in the cards for 2024. It’s becoming increasingly more evident that we are in a period of fiscal dominance, I am not sure that monetary policy is having as much of an effect outside of residential and commercial real estate. The former is holding up fine in the face of limited inventories while the latter is holding on for dear life; they stare down the barrel of a gun in the form of refinancing. Always good to zoom out a little. I am not sure we will see those prices come down without a deep recession, but before we do too much hand wringing it’s important to put things into the proper perspective. For the last 30 years, dating back to 1994, CPI has average just below 2.50% including the recent the elevated inflation, that’s less than half the inflation for the 30 years from 1966 through 1995 where prices grew at a clip of over 5.4%. Magnificent 7, 6, 5 4, 3 , 2, 1… Aside from Meta and Nvidia the latter of which has somehow managed to add an 80% return on top of a truly breathtaking 2023 performance, we have seen quite the dispersion in the returns and what appears to be a case of returning from orbit for high flying Apple and Tesla. With the group trading at a forward P/E ratio of 31 times there is no room for error as they trade at 50% premium to the S&P itself over which they have a great influence given their size. What is even more amazing is that they trade at a 100% premium to the equal weight index. Something has to give, is it that Amazon, Microsoft, Meta and Alphabet starts to resent buying GPUs from Nvidia with 80% gross margins and they start in house fabrication much like Apple did with ditching Intel in 2020. Rent seeking behavior is usually short lived as competitors look to take share as well. Or perhaps it’s all that enterprise spending that doesn’t yield the earnings growth forcing multiples to contract. Much like the upcoming NFL draft there rarely is a can’t miss story out there. Much like “retired” Bill Belichick did at the helm of the New England Patriots for 20+ years, perhaps trading down and having more picks allows you to build a better roster versus needing everything to go right with your one great idea. Diversification and identifying mispricing is a consistent path to wealth even if it takes you a little longer to get there. Common prosperity or conciliatory China? Polishing off the old playbook and rebranding communism by using some more gentle words like common and prosperity doesn’t mean your people have to like it. History suggests that there is nothing common about prosperity when the state dictates distribution of resources as was the case for the 30 years under Chairman Mao until Deng Xiaoping ushered in market based reforms in the late 1970s and early 1980s. Clearly Xi Jinping’s admiration of Mao Zedong’s emphasizes his cult of personability and despotic tendencies while minimizing the fact his policies resulted in the deaths of millions of Chinese whether by famine or the Cultural Revolution. But the Chinese have had their taste of capitalism it appears they like what they experienced. While the property problem persists, efforts to cool tensions between the US and Chinese relations along with more aggressive and targeted stimulus may break the years’ long malaise. The last pre-pandemic slowdown in China required about 2 years to run its course and then set up a period of synchronized global growth from 2016-2019 a similar recovery would be welcome as trade may provide further disinflationary pressures as they compete with Mexico and India for labor and any increase in consumption is bound to help US multinationals grow earnings after the US consumer eventually slows down. We are not ready to pivot away from our view China is practically un- investible but this is modestly constructive and worth monitoring. Virtuous cycles of asset allocation based investing. Whether the calendar dictates adjusting your investment mix or there is more discipline based on drift and data, the fact we have spent 30 of the last 40 years in one heck of a bull market has meant that there has been an unquenchable demand for fixed income. At one point the bond market in the US dwarfed the stock market but stocks have caught up where both pools of capital valued at about $51TT. Globally the bond market is a bit bigger than the equity markets, $133TT to $110TT. Rates have been coming down since the early 1980s only to have increased a bit in the middle of the 2000s and again most recently. Higher rates should attract more buyers, yet $6TT is parked in money market funds. The average bond buyer has become much more price (yield) insensitive, buying bonds in something resembling rote behavior. If the market continues to go up and likely at a rate of change that exceeds the bond market, and it should given the uncertainty associated with owning stocks and the natural inflationary forces that drive asset prices higher, then we should more often than not have a bid putting something of a lid on yields and not needing to implement a Japan style yield curve control. Mark Twain’s famous quip about his death being an exaggeration seems fitting for all those folks. Please join us April 18th for our Quarterly Market Review and Outlook. Register Now Sources: Baron’s WSJ, BLS, ISMForbes, JP Morgan Asset Management Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website, www.adviserinfo.sec.gov. Past performance is not a guarantee of future results.

It’s February already, thankfully. The sun seems to be on extended holiday in the Northeast. Perhaps Punxsutawney Phil will be more accurate than economists and strategists alike as this morning he indicated an early Spring is in store. As for us market watchers experiencing something akin to Groundhog’s Day would be nirvana and the first month of the New Year was a continuation of the final two months of 2023. So far, so good for February too. With the S&P logging a return of 1.68% for the month, that annualizes out to a 20% return, ahh, if it were only that easy. There has been a lot to unpack, so we’ll meander across a number of topics to share our thoughts and what we are looking at right now and in the months ahead. Central Banks: As we have joked about recently, Federal Reserve meetings have become must-see TV. For the last 6 months, since the last hike in July, the meetings have been less about the rate announcement itself and more about trying to get inside Chairman Powell’s thought process. With markets hanging on every word and probing the quarterly Statement of Economic Projections (SEP) for any insights, it’s no surprise that two of the Fed meetings in 2023 corresponded to the most volatile trading days of 2023. The presser earlier this week augured the worst day since September when Powell seemed to take the March cut off the table. Data since then only strengthened the case for May as the lift off date for their easing cycle. That seems to be reasonable enough, in acknowledging that they have come a long way in taming inflation (rolling 6 month PCE is around 2%) they can start to shift focus to the other part of their dual mandate, which is full employment. Bringing both inflation and jobs into a more balanced weighting is a good thing and a far cry from the pain Powell mentioned in August 2022 at Jackson Hole. While Chair Powell and the Fed are the most important game in town, central banks in the UK, Europe and Japan are worth monitoring. The UK and Europe are dealing with more of the stagflation dynamic we witnessed in the late 70s, though there have been some recent signs of easing inflation. The ongoing impact of higher energy prices has more impact there where they rely heavily on imports and the fact their mortgage rates tend to be much more variable in nature have meant higher monthly payments not just for new buyers but even those who have purchased homes 5 or more years ago. In the States, it’s far more common for borrowers to term out their debt for 30 years. Many folks with a mortgage today have locked in rates of 4% or below. Monetary policy likely will have some impact over the next several years and I would expect the trough of their easing cycle to be below that of what we see in the US. The ECB seems likely to wait for the United States to move first, but they won’t be far behind. Japan has witnessed sustained inflation for the first time in more than 30 years but at a much more palatable level. They have thus far maintained yield curve control policies which suggests that they are in no rush to start raising rates. If they do it’s likely to be modest at best as with households having sizable exposure to the JGBs any drop in price brought on by higher rates may impact consumer behavior. Higher rates would also have some real impact on the carry trade, but that discussion is for another day. Labor: As the frequency of layoff announcements hitting the headlines have increased over the last 12 months the Fed needs to be very careful about how much softening occurs before it becomes difficult to reverse that trend. Fortunately after a blockbuster January Nonfarm Payroll Report, the unemployment rate ticked back down to 3.7% after rising the prior month albeit slightly to 3.8%. It’s becoming ever more obvious that so goes the labor market so goes the economy. When the unemployment rate jumps by .50% in a short period of time, it’s likely to rise another 1.00% in a hurry as we have seen in prior cycles leading to a recession. Allowing the labor market to get untethered is the quickest path to a hard landing. We have seen new weekly unemployment filings increase to 224,000 in the most recent week and continuing claims remain around 1.8MM. Hardly worrisome levels unless you are one of those impacted, but the direction itself is worth watching. It was good to see job openings surprisingly increase in the most recent JOLTS report and especially in sectors like manufacturing. Another bright spot is that the “quit rate” has dropped sharply since the height of the pandemic where workers bounced to new opportunities at an unprecedented rate speaking to labor tightness. This probably has an added positive effect on productivity as fewer new workers have to adjust to unfamiliar surroundings. Continuing the soft landing narrative the Bureau of Labor Statistics just released their quarterly Employment Cost Index which showed further moderating, which is a good sign when it comes to inflation and margins. Nominal wage growth is around 4% back to levels we saw pre-pandemic. Inflation: With CPI trending down, and PCE following a similar path perhaps the debate over transitory can be put to rest. The stickier shelter component will start to show signs of disinflation or outright deflation in the coming months as softer housing data and a glut of new multi-family housing comes online. While there has been much hand wringing over financial conditions easing (whether directly or indirectly), there is little evidence that higher asset prices are inflationary when it comes to consumption of goods or services. In the post Global Financial Crisis(GFC) world of Zero Interest Rate Policy (ZIRP) inflation consistently undershot the Fed’s target. I am not convinced this time is different. The situation in the Red Sea is worth monitoring, but that shipping lane has less impact on goods that come into the US versus other countries and the case for strong case for continued globalization means large export driven economies like China, Vietnam, Mexico and increasingly India are able to provide disinflationary if not deflationary pressures at a time when that may not be a bad thing. Consumer sentiment surveys have for the last couple of years suggested inflation expectations had become anchored somewhat higher, but some better responses over the last couple of months are encouraging. Earnings & Margins: As we are in the midst of 4th quarter earnings it would be best to describe the current numbers as “meh.” Profits are likely to be up quarter over quarter for the second quarter in a row, but have thus far come in lower than estimates going back a few months. Some of that is a byproduct of companies being very cautious and not taking on excess inventory, worried about their end consumer and some margin pressures remain. According to FactSet’s Earnings Insight as of Friday January 26th of the 25% of companies that had reported roughly 70% of companies have beat on both earnings and revenue, below 3 and 5 year averages respectively. This week we have seen some better than expected earnings from names in the Technology, Consumer Discretionary and the Communication Services sectors which have an outsized weighting on the market so the overall numbers are likely to improve but all in all it’s hardly been a blowout quarter. Given present lofty valuations, meaningful moves higher from here will need to be supported by improving earnings growth. While the consensus estimate called for as much as 14% YOY growth for the S&P 500 as recently as last Fall, those numbers have come down now to about 10% for 2024. That figure may still be a bit ambitious with GDP forecasts for the year roughly around 2% and inflation moderating. We know companies have a number of levers to pull to improve earnings from buybacks to layoffs, the former an accounting maneuver while the latter likely having more negative intermediate impact on the economy as a whole, so be careful what we wish for here. The good news is that margin pressures are likely to abate given further improvement in the supply chain, improved productivity and slowing wage growth. We may not see peak margins like we saw in 2021 however they remain historically high which makes sense in a less capital-intensive economy. Global Economy: As we alluded to the challenge of central banks all around the globe to find that happy balance on policy, it’s safe to assume some positive developments abroad would be a positive for the US economy which has run above trend for the last couple of quarters. While there was hope for an improving China in early 2023 and the possibility of a real slowdown in Europe could be avoided, that was not the case. As China continues to wrestle with a housing crisis that has been going on for nearly 10 years, structural reforms have been delayed as Xi Jinping focuses on the common prosperity initiatives which have hurt markets at home. At this point the base case should assume very little help from China in supporting global growth and that seems to be well priced in. If there is some improvement it would be welcome, though I wouldn’t bank on it. Europe, China’s largest trading partner, sees it’s trajectory far more closely tied to developments in the Middle Kingdom, they may not move in lockstep but it’s unlikely that you’d witness a reacceleration in growth in one and not the other. Fortunately, valuations abroad are far less demanding, though markets likely exceed expectations. The likelihood of lower interest rates and possibly a weaker dollar would be a positive for US investors investing abroad as well as remove some near term headwinds on emerging economies that still very much rely on dollar funding for their credit markets. In summary, a repeat of the last couple of quarters would be great where it’s been upside surprises for both the economy and the markets here in the US. As inflation continues to head lower, that’s a positive even if growth may have peaked in the 3rd quarter of 2023. Growth above trend (2%+ in real terms) is supportive of the labor market and asset prices and if some of the encouraging data regarding manufacturing is not in fact a false start we could revert back to synchronized global growth like we saw in 2016-2017. They say we’re young and we don’t know We won’t find out until we grow Well I don’t know if all that’s true’ Cause you got me, and baby, I got you -Sonny & Cher Get In Touch Sources: WSJ, Barron’s, Factset, Bloomberg, YCharts, FRED St. Louis Fed, Bureau of Labor Statistics

Your financial plan can weather times like these, make sure your emotions don’t get the best of you.