Financial Literacy

Navigate college funding without compromising retirement. Expert guide to balancing multiple funding sources, avoiding debt traps, and protecting your family's financial future.

Financial Literacy Is Not Enough and Why Strategy is the Real Differentiator in Today’s Wealth Shift

Women now own 39% of U.S. businesses and are growing wealth at 8.1% annually. Discover why strategic planning—not just financial literacy—drives real wealth building.

Most young workers lose thousands in unvested 401(k) matches. Learn the 5 vesting schedule types and how timing job changes can save your retirement.

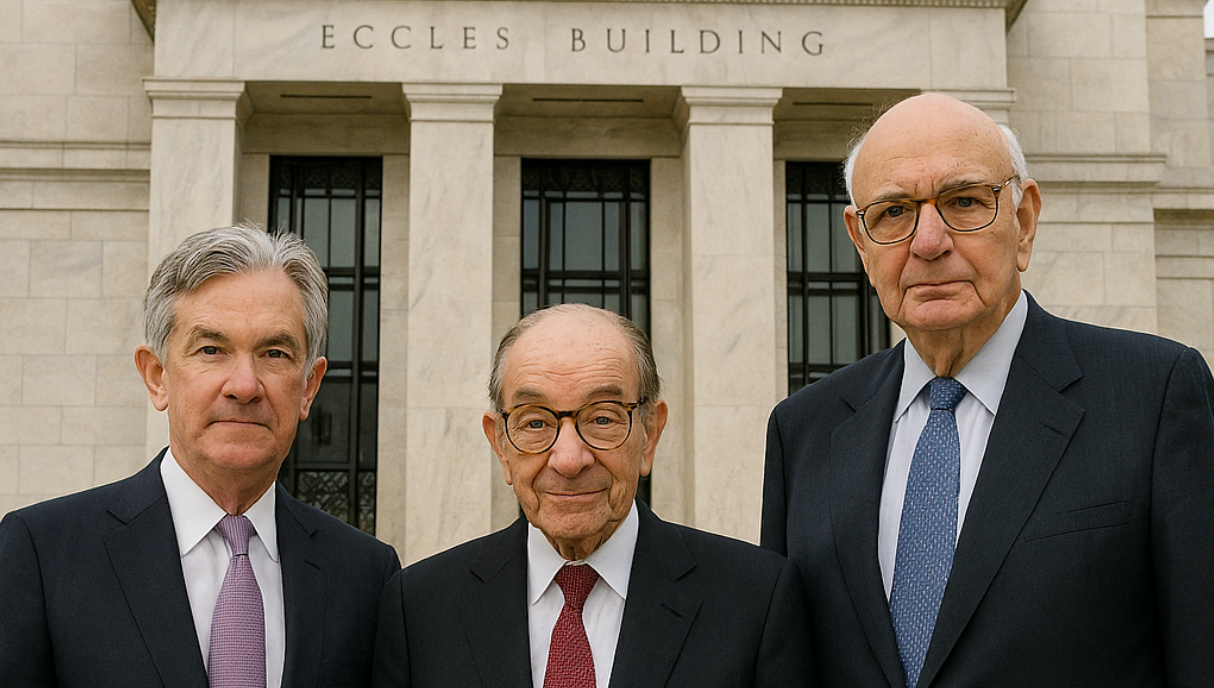

How the Federal Reserve's operations impact finances. Explore the roles of Fed governors, banks, and FOMC—plus what Jerome Powell's policies mean for your money.

Learn about the US Federal Reserve System's structure, history, and current leadership. Understand the Fed's dual mandate, FOMC meetings, and how Fed policy decisions impact investors and consumers.

Open enrollment is traditionally seen as the time to reassess your health insurance options, but with the employment landscape becoming more competitive, many companies are expanding their benefits packages. Employers are now offering perks such as legal assistance and gym reimbursements, among other appealing options, that employees should carefully consider. It’s also a key opportunity to review your financial benefits, as employers might provide additional life or disability insurance at a much lower cost than you’d find on your own, often with the option to keep coverage if you ever leave the company. Here’s what you should keep an eye on from a financial standpoint: Health Insurance Costs: Health insurance remains the most recognized aspect of open enrollment and one of the most crucial. Compare various plans by looking at monthly premiums, deductibles, maximum out-of-pocket limits, and coinsurance. Your goal should be to choose a plan that balances your medical needs with your budget. Tax-Advantaged Accounts: Health Savings Accounts (HSAs) are linked with high-deductible health plans (HDHPs) but are worth considering due to their unique tax benefits. For 2024, HSA contribution limits have increased to $4,150 for individuals and $8,300 for families, up 7% from last year. Unlike the “use it or lose it” nature of Flexible Spending Accounts (FSAs), HSA funds can roll over year after year, grow tax-free, and withdrawals for qualified medical expenses are tax-exempt. This triple tax advantage makes HSAs a powerful tool for managing healthcare costs and even long-term savings. The trade-off is the higher deductible and out-of-pocket expenses typical of HDHPs, which can be around $3,000 and up to $6,000-$8,000, respectively. Understanding these differences is essential for making the right choice. Retirement Contributions: Open enrollment is an ideal time to review your retirement contributions. For 2024, the contribution limit for employee contributions to 401(k) plans is $23,000, with an additional $7,500 catch-up contribution for those 50 and older. Increasing your contributions, if possible, can help secure your financial future. Employers may also permit “after-tax contributions,” which can be converted to a Roth IRA, enabling tax-free withdrawals later under specific conditions. Many employers default employees into target-date funds, but these may not suit your personal risk tolerance or financial goals. We often adjust our clients’ retirement portfolios to better align with their individual circumstances. Be sure to take full advantage of any employer match and ensure your investment strategy is consistent with your long-term objectives. Life and Disability Insurance: Most employers provide basic life insurance coverage equal to 1-2 times your salary. Depending on your family’s needs and financial obligations, you may want to purchase additional coverage. Employer-provided term life insurance is often cheaper than what you’d find on the open market and can sometimes be continued if you leave your job, though the cost might increase. Consider your financial obligations, such as income replacement, childcare, and funeral costs, when determining your needs. Similarly, evaluate your disability insurance coverage to make sure it’s adequate and explore supplemental coverage if necessary. Dependent Care Expenses: Many companies offer Dependent Care FSAs, which allow you to set aside pre-tax dollars for child or elder care expenses. However, keep in mind that you cannot use the same expenses for both the Dependent Care FSA and the Child and Dependent Care Tax Credit. Choose the option that provides the greater tax benefit based on your situation. Overall Financial Impact: It’s important to consider how each benefit impacts your overall financial picture and aligns with your budget. Benefits can quickly add up in cost, so ensure you have a sufficient emergency fund—ideally 3-6 months of expenses—held in a high-yield savings account or money market fund. Simultaneously, plan for long-term financial goals, such as retirement, home buying, education funding, and other significant life events. Balancing these priorities can be challenging, but it’s necessary to build a solid financial foundation. Open enrollment is a valuable time to fine-tune your benefits package, helping you work toward your financial goals and safeguard your family’s future. Carefully evaluate all the options available and consider seeking advice from a financial professional. Our clients face unique and complex financial situations, and we assist them in navigating these challenges by providing clear goals and actionable steps. Partner with an advisor who helps you feel confident in your financial planning and work towards your personal vision of financial freedom. Additional information, including management fees and expenses, is provided on our Form ADV Part 2, available upon request or at the SEC’s Investment Adviser Public Disclosure website, https://adviserinfo.sec.gov/firm/summary/321097 . Past performance is not a guarantee of future results.

We have been seeing record-setting numbers with the Mega Millions prize climbing towards $1.55 billion, getting closer and closer to setting an all-time record high. The last time we saw numbers this high was from a winner in October of 2018 taking home $1.537 billion . Anytime someone comes into newfound wealth, it’s an exciting yet unnerving feeling as people are overwhelmed with decisions they thought they would never have to make and the age old questions around maintaining your wealth before you spend it all. After all, 68% of the US economy is driven by consumer spending, however, studies are mixed showing some lottery winners of more than $200,000 in earnings have had their lives positively affected, while a more disputed study shows inherited wealth of people in their 20s, 30s, and 40s spend roughly half of their inherited wealth within a few years. Regardless, let’s take a look at how to keep yourself and your wealth happy. In initial discussions with our clients, we delve into determining their hurdle rate – the threshold at which they can achieve their objectives, or the minimum rate of return essential for progress, all while minimizing undue risks. If they desire more of a return on their investments, we discuss the difference between needs and wants. Anything above their desired rate of return tends to turn into excess. That story never ends well, which is why it is extremely important to flush out your personal life goals with a financial professional, attorney and accountant. What amount of money will let you go on idyllic vacations you can now afford, give to family or charity, upgrade to your Barbie dream house or finally get that Equinox membership? An accountant is an important piece of the puzzle because after subtracting the cost of your ticket you owe federal and state (depending on where you live) income tax on the rest. I know, the IRS was not on your list of friends or charities, but their piece of your pie is an important number to consider. Right away, the IRS withholds 25% but depending on how much you win, you may still owe more the following April when you file. Just to give some context, that is $375 million you’re giving back to Uncle Sam as soon as you win. Considering top federal income tax brackets are 37% which is an additional $180 million, it’s a check you want to know you are writing sooner rather than later as you go forth in figuring out what your new financial future holds. Depending on where you live, your state may have their hands out on earnings too. For all our New Yorkers out there paying an additional 13% in state income tax, if you think just because you went to NJ for the winning ticket and the earnings were paid out there, think again. You will owe your state of residence at tax time but will receive a credit for the amount you already withheld in the ticket winning state. After winning the lottery, one is faced with the choice of lump sum earnings or a series of monthly payments (also known as annuitizing payments). Which one is better? The answer is a personal question but also a question about time value for money. If you take the annuitized payments, you spread the tax liability over a certain number of years but if you are going to invest a portion of your winnings, investing a dollar today may be worth more than investing a dollar 5 years from now. Taking a lump sum payment now also allows you more control over your assets in creating a plan that meets your immediate (3-6 months), intermediate (3-7 years), and long term (10+ years) objectives. It’s also important to consider how your assets are growing. We refer to this as asset location. Make a plan that allows for a portion of your assets to grow tax free (like a Roth IRA), tax deferred (Traditional IRA or low-cost variable annuity), and standard brokerage assets that are taxed on capital gains and interest income or dividends. Make your money work as hard as you do while being as efficient as possible. Winning the lottery or inheriting large amounts of money can be absolutely life changing and put you on a completely different life trajectory than you ever thought possible. No matter how large your winnings are they are not infinite, so put yourself on a path to achieve exactly what you want in your life. Take control by surrounding yourself with the right group of people who are going to get you there. Get In Touch The views expressed represent the opinions of Breakwater Capital Group and are subject to change. These views are not intended as a forecast, a guarantee of future results, investment recommendation, or an offer to buy or sell any securities. The information provided is of a general nature and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person. Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website. https://adviserinfo.sec.gov/ Past performance is not a guarantee of future results.

An emergency fund acts as a financial buffer and serves as a safeguard against unforeseen expenses like job loss, car repairs, or medical bills. Its utility stems from its capacity to shield you from falling into debt, while simultaneously offering the invaluable security of being well-equipped to confront any unforeseen events that may arise. Here are some of the benefits of building an emergency fund: Avoid debt: If you don’t have an emergency fund and you have an unexpected expense, you may be tempted to use a credit card or take out a loan to pay for it. This can lead to debt, which can be difficult to pay off. Many credit cards have variable rates of interest and can make the unexpected debt much more expensive. Peace of mind: Knowing that you have an emergency fund can give you peace of mind knowing that you’re prepared for unexpected events. This can help you sleep better at night and can reduce stress levels. It is often a great first step in becoming financially independent or taking back control of your financial situation. Improve your credit score: Having an emergency fund can improve your credit score. This is because lenders look at your debt-to-income ratio when they’re considering you for a loan. If you have a high debt-to-income ratio, it’s a sign that you’re struggling to make your monthly payments. Having an emergency fund can help you reduce your debt-to-income ratio, which can improve your credit score. The amount of money you need in your emergency fund will vary depending on your individual circumstances. However, a good rule of thumb is to have three to six months’ worth of living expenses saved up. This will give you enough time to find a new job or pay for unexpected expenses without having to go into debt. In the case of a job loss, three to six months’ worth of savings can also help you to avoid dipping into an old 401k or a Roth IRA account which may both have penalties associated with a distribution. Here are some tips for building an emergency fund: Start small: If you’re not able to save a lot of money each month, start by saving a small amount. Even saving $50 per month will add up over time. Automate your savings: Set up a monthly automatic transfer from your checking account to your savings account. This will help you make saving money a habit and if these funds are in a separate account, you are much less likely to dip into that amount to pay regular monthly expenses. Find a high-yield account: There are many high-yield savings accounts or money markets available that offer higher interest rates than traditional savings accounts. This can help your money grow faster. Don’t touch your emergency fund: The only time you should use your emergency fund is for unexpected expenses. If you become tempted to use it for anything else, you’ll have to start saving all over again. According to Bankrate’s annual report, only 48 percent of U.S. adults say they have enough emergency savings to cover at least three months’ worth of expenses . Building an emergency fund is an important financial goal. By following these tips, you can start building your emergency fund, take control of your financial situation, and protect yourself from unexpected expenses. Maintaining an emergency fund is crucial due to its role as a financial safety net. Beyond its pragmatic utility, an emergency fund also grants a peace of mind, ensuring preparedness and resilience in the face of unpredictable events, ultimately fostering greater financial stability and security for the future. Get In Touch The views expressed represent the opinions of Breakwater Capital Group and are subject to change. These views are not intended as a forecast, a guarantee of future results, investment recommendation, or an offer to buy or sell any securities. The information provided is of a general nature and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person. Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website https://adviserinfo.sec.gov/ Past performance is not a guarantee of future results.