Money

Learn when wealth-building discipline becomes counterproductive. Expert guide to balancing saving for the future with enjoying life today through smart financial planning.

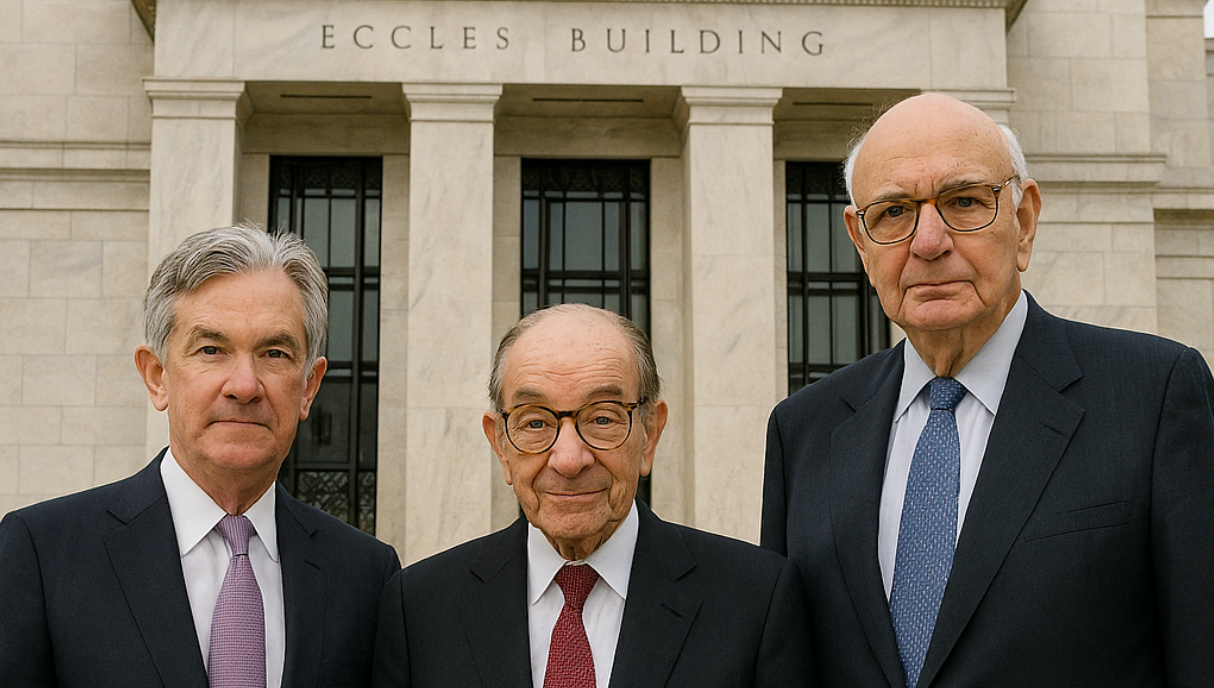

Fed Chair transition May 22, 2026: Powell's final decision, Warsh's hawkish monetary policy changes. Iran war complicates Fed handoff. Market analysis.

Financial Literacy Is Not Enough and Why Strategy is the Real Differentiator in Today’s Wealth Shift

Women now own 39% of U.S. businesses and are growing wealth at 8.1% annually. Discover why strategic planning—not just financial literacy—drives real wealth building.

Market outlook 2026: Geopolitical tensions drive oil prices, AI infrastructure spending concerns, private credit risks. Analysis of Q1 performance and outlook.

Foreign investors poured $1.55 trillion into US assets in 2025—not selling America, but rotating from bonds to stocks. Discover why global diversification is now essential for investors.

Expert financial planning for high-net-worth divorce. Learn strategies to protect assets, navigate complex property division, and ensure equitable settlement outcomes.

Strategic gifting can reduce estate taxes and help loved ones when they need it most. Discover 2025 gift tax rules, state exemptions, and planning strategies.

How the Federal Reserve's operations impact finances. Explore the roles of Fed governors, banks, and FOMC—plus what Jerome Powell's policies mean for your money.

Learn about the US Federal Reserve System's structure, history, and current leadership. Understand the Fed's dual mandate, FOMC meetings, and how Fed policy decisions impact investors and consumers.