Sold on America: Why U.S. Assets are a Story of a Longer-Term Rotation, Not Rejection

Written by James Fonzi, CFA®

After World War II, borders for the trade of real goods and financial products became ever more permeable, and as a result, the global economy has become deeply integrated to a degree never seen before; a trend that looks set to persist despite the talk of deglobalization. More recently, in the aftermath of the Great Financial Crisis, the United States was one of only a handful of countries that experienced a lasting economic recovery and healthy expansion. Whether the cause or effect, this meant US markets were a destination for American savers and foreign capital in search of attractive returns, especially in an era of financial repression. But more recently, there have been some fissures in the narrative of free markets, and there are potential disruptive catalysts that by now should be familiar to us all as investors: the explosion in the development of Artificial Intelligence (AI) is reshaping industries and possibly the labor market along with it, rising geopolitical tensions, lofty asset valuations, and fiscal concerns exacerbated by a weakening US dollar and above target inflation. What may have solely been considered concerns for the “permabears” in the past have lately become top of mind for investors both at home and abroad. Starting in the second half of 2024, continuing into 2026, US investors have become more comfortable investing abroad, and foreigners are less willing to recycle their dollars back into our capital markets at the same pace, which begs the question: Are investors in fact ‘Selling America’?

Policy signaling has played a part, with the administration embracing a weaker dollar or talks of a Mar-a-Lago Accord, but that seems too simplistic an explanation alone. A variety of factors are contributing to a growing appetite for investors seeking the optimal risk-adjusted returns. Demographics, market fundamentals, and interest rates are also contributing to the willingness to venture away from the standard fare.

Foreign markets have delivered intrigue and recently impressive results, while US markets, perhaps victims of their own past success, have prompted more questions than answers. Despite the sensational headlines that suggest dollar assets are being dumped in droves, the real data suggest investors are not running from US assets, but rather their approach is evolving. It is a story of rotation rather than rejection, a structural shift. All that to say, a global approach to investing is now more critical than ever. Fortunately, a robust investment landscape offers investors compelling opportunities here and abroad, if they are willing to do the work. Our view is that investors remain sold on America, but their palate is evolving. Enough on the talking points, this story is better told through numbers.

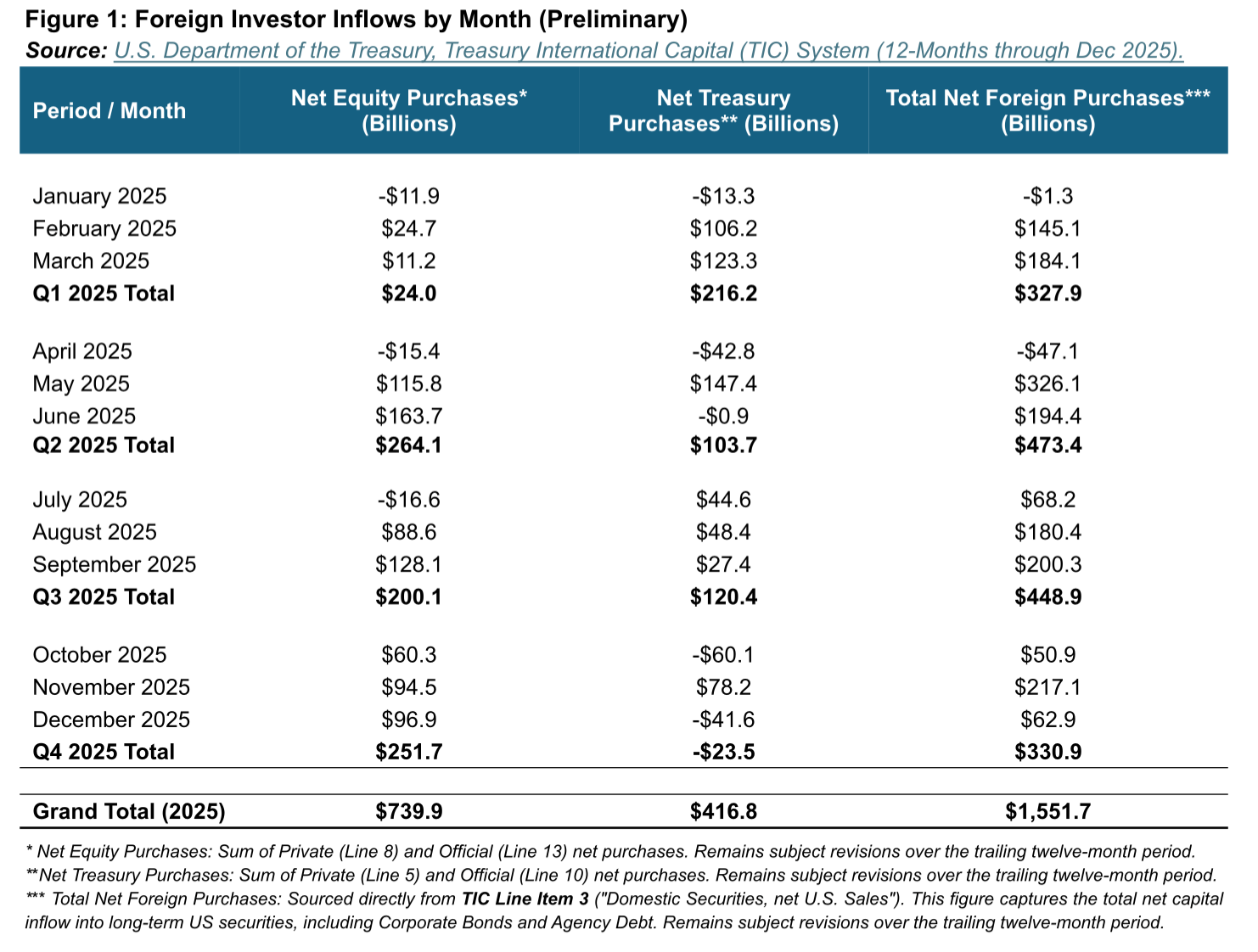

The Hard Data: a $1.55 Trillion Vote of Confidence

Contrary to the bearish ‘Sell America’ rhetoric, global capital is not fleeing from the United States but rather embracing it. US assets experienced a net inflow of $1.55 trillion from foreign investors over the course of 2025 (see Figure 1 below), an increase of approximately $370 billion when compared to $1.18 trillion of net inflows in 2024. Net inflows remain robust, even maintaining positive momentum into the end of the year in December, despite meaningful outperformance for overseas stocks and bonds to close out the year. “Performance drives flows,” as the saying goes. Perhaps that’s true, and there may be a lag here as investors absorb incoming data, but investors remain cautious, having been fooled by the occasional head fake over the last two decades. You’d have to go back to the period from 2002-2006 to see a sustained period of outperformance from ACWI ex-US vs. the S&P 500. While foreign markets seem ripe for a similar stretch of outperformance, investors seemingly aren’t fully convinced, as evidenced by their capital allocation decisions.

By focusing on Long-Term Securities rather than total capital flows (which are inclusive of short-term banking activity and can cloud our longer-term strategic view), we see foreign investors are tipping their hands. They are, in fact, sellers of US debt but buyers of US growth, with a clear rotation out of treasuries and into equities at an almost 2-to-1 clip in 2025 ($740 billion to $417 billion). But foreigners were not selling all debt instruments; they had net capital inflows into US credit and agency debt markets to the tune of approximately $420 billion. Investors are buying the entire US capital stack while rotating out of US government debt.

Interestingly, the composition of foreign wealth in the US has also flipped over the past 15 years. In mid-2009, approximately 27% of long-term securities holdings in foreign investor portfolios were allocated to US equities. Allocations to US equities as of June 30, 2025, have grown to approximately 56% of all foreign long-term US securities holdings, driven by both compounded growth and increased rotation into equities. This is clearly not a

capital flight, but rather a bet on the US economy’s resilience – it is risk on. With this backdrop in mind, it is also important to address the cause of the growing global aversion to US treasuries. The headlines will say it’s politics, and to a degree it is, but the structural forces that have catalyzed this shift far outweigh political influence.

US Treasuries for Sale: Structural with a Side of Political

As the global rotation into US equities continues, the rotation out of US Treasuries is often mischaracterized as solely geopolitical spite. This is not a false claim and some of the selling is certainly driven by tariff volatility, uncertainties around fiscal policy, and the volatile messaging from US President Donald Trump and his cabinet. The reality, however, is far more mechanical and involves some broader structural shifts. Much of the selling is driven by revised Pension Structures around the globe, the mechanics behind Hedged Yields, and Central Banks seeking Diversification. We will discuss each of these in further detail and provide some illustrative context along the way.

- The Pension Shift and a Fading “Structural Bid”

For several decades, many global pensions have been structured as Defined Benefit (DB) Plans where participants receive a guaranteed payout at retirement. These payouts are long-term liabilities for the sponsor; they inherit a lot of long-term funding risk. In attempting to offset this risk, DB pension plans used what is referred to as Liability Driven Investing (LDI). LDI is a framework followed primarily by market participants such as Insurance Companies and Pension Funds, who invest assets strategically to meet future liabilities (often longer term). Thus, DB plans had to buy long-duration US bonds (10yr – 30yr) and other long-term sovereign bonds to match their future long-term payment streams, regardless of market prices and yield levels. There has been a recent shift, similar to what took place in the early 1980s in the US with many sponsors switching to a Defined Contribution (DC) pension structure where an employer and employee generally contribute to the plan and future payouts are not fixed and are tied to investment performance, thus shifting a large share of the risk from the sponsor to the employee. The natural outgrowth of such a shift is greater equity exposure. As of late 2025, DC plans now control approximately 63% of global pension assets (compared to 41% just two decades ago) 1*. Another catalyst for the shift away from long-term bonds is that major DB markets (UK, Netherlands, Japan) have matured. They are now paying out retirees, and as they make such payments, they are net sellers of assets as the duration of their liabilities continues to shorten. In contrast, “new” capital flows from contributions into DC plans allocate significantly less to long-term sovereign bonds. The “automatic bid” for the long end of the US yield curve has been evaporating with a new reliance on price-sensitive buyers (hedge funds, asset managers, mutual funds, etc.) rather than regulatory-driven capital (pensions). Long-term sovereign bonds around the world are feeling this pain, not just US treasuries.

2. Staying Closer to Home: The Preference for Local Bonds

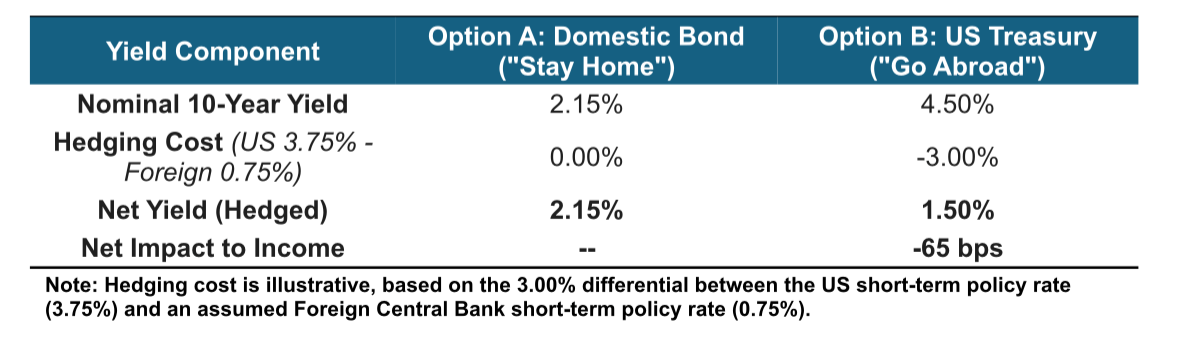

Local bonds have been a central topic in fixed income markets over the past year as the subsector has experienced broad outperformance against US issued bonds. Additionally, inflation differentials between emerging and developed economies have converged in tandem with a weakening US dollar. Despite the plethora of variables, the math here is simple. As an example, let us observe a hypothetical foreign life insurer deciding between purchasing a long-term domestic bond versus a long-term US Treasury to meet future long-term liabilities. When it comes to investing in foreign bonds, domestic investors care less about the nominal yield and rather more about the yield after hedging currency risk and its associated costs. In the current landscape, hedging costs are closely tied to central bank policy rates (i.e. the Federal Funds Rate) and these rates are considerably higher today than have been over much of the last 25 years, particularly domestically. Unlike diversification, the only free lunch in investing, this can be an expensive endeavor and investors are reacting accordingly. Recent events such as the Japanese carry trade blow up in August of 2024 has compounded a degree of additional risk premia to hedging costs as well.

Below is a brief mathematical illustration (all values are illustrative only):

Conclusion: It’s purely mechanical. There isn’t capital flight in the US Treasury market so much as US bonds simply yield less now and the insurer in this example would not risk 65 basis points (bps) in losses to income if it can avoid doing so. Interest rates change daily and structural changes like this are temporary when considering the longer-term picture. For example, if the FOMC decided to cut US short-term rates aggressively and the yield curve steepened, then the risk-reward trade-off laid out above changes and may immediately favor the foreign investor buying US Treasuries.

3. Central Banks Have Gone Shopping

Central Banks around the world are reacting to global shifts in policy and trade. These are public institutions, and thus they are less sensitive to yields as many support the management of a nation’s currency, money supply, and monetary policy in pursuit of economic stability. They are less sensitive to yield and more so to liquidity and diversification. Given longer-term fiscal pressures and monetary policy uncertainty in the US, many foreign central banks and public institutions are selling treasuries and bolstering their strategic reserves of gold with the proceeds. Gold is seen as safe for many Central Banks as it doesn’t involve counterparty risk (in its physical form, that is). Many central banks are also more focused on short-duration assets as such assets are most effectual in monetary policy implementation. This again has been a pervasive structural theme as almost 60% of U.S. Treasury securities held by foreign investors are now held by private investors such as pension and mutual funds, which has been a trend for over a decade-plus.

As investors with a global view the case for the US is still a strong one and as we can see is broadly structural more than anything else, however, it is imperative to expand on why capital (domestic and foreign) is finding new homes in new markets. Our palate is expanding.

(1* The study covers the P22, which isthe top 22 pension markets in the world by aggregate assets (accounting for an estimated 92-96% of all global

Global Context: Opportunities without Borders

US risk assets remain the main course for global investors, but the side dishes have become increasingly attractive. This shift is healthy and is a bid to diversification driven by specific structural improvements abroad. And it is visible across the globe. Japan and Korea serve as recent examples of improved corporate governance and favorable economic regime change, drawing investors to their markets. Taiwan is a mature market at the center of semiconductor production while posting strong GDP growth and low inflation. India is an emerging market leader in GDP growth, a growing middle class, and is undergoing a digital transformation paired with more robust consumer demographics. Europe has positioned itself as a story of stability, strong

governance, and as a global leader in luxury goods. Despite bureaucratic headaches that have plagued the EU in recent defense pursuits, defense spending has been a massive draw for foreign investors. Latin America finds itself at the center of the critical minerals and energy transition race, while also ushering in a tech boom and nearshoring opportunities for North American economies. In addition to the exciting global themes, simple mathematics is at play. The valuation gap between US equities and foreign equities has drawn loads of global capital as well. The investment universe is teeming with real-world examples, but for brevity, we will focus on two brief topics that have been top of mind for investors in 2026.

- The “Governance Premium” in Japan

Along with buying Japanese equities and debt, investors are also buying reform. Japan’s “Sanaenomics” agenda, an effort to spur fiscal expansion and foreign direct investment, has foreign capital flooding into Japanese capital markets. The mandate that companies must trade above book value has unlocked a wave of imminent and expected future share buybacks. The Nikkei, Japan’s largest equity index (price-weighted composite of the largest 225 Japanese companies), has stormed out of the gates posting a return of almost 7% since the start of 2026 (2*) (until recent market volatility, the index had returned ~16%). Monetary policy looks accommodative under the new regime ushered in under Takaichi Sanae and thus has investors excited for Japan’s long-term growth prospects. The capital flight to Tokyo is a long-term bet on shareholder returns in a market that has been starved of them for the past decade-plus.

2. The Valuation Gap: Balancing Perfection and Safety (3*)

Research from J.P. Morgan Asset Management highlights a historic valuation gap between domestic US markets versus foreign markets. As of the end of 2025, the SP 500 Index had a forward P/E of approximately 22.0x (versus a 30-year average of 17.1x). Turn to broad emerging markets, Japan, the Eurozone, and China, and valuations are presenting much more attractive entry points. For example, broad emerging markets posted a forward P/E at the beginning of 2025 at 12.0x, which was also the 20- year average at that time. This multiple has expanded to 13.4x by the end of 2025, signaling the growth in capital flooding into these markets. At the end of January, the forward emerging market P/E was 13.0x. This has also been paired with earnings growth as well, and thus is not simply a melt-up in price expanding the multiple. Similar behavior can be seen in the Eurozone, where forward P/E stood at 12.9x at the beginning of 2025 and expanded to 14.9x by the end of the year, again bolstered by capital inflows and earnings growth. The relative value equation provides a logical answer. The US is a bet on earnings growth and priced to perfection; foreign markets are priced with a margin of safety and the prospect of multiple expansion.

The story of reform and valuation will continue to evolve as the global economy becomes more integrated and the gap between emerging and developing markets narrows. This looks to be a display of conviction over the longer term than a temporary chase for returns.

(2* Return data as of March 12, 2026. Source: Bloomberg.)

(3* All data contained or derived from J.P. Morgan Asset Management Guide to the Markets, U.S. | 1Q 2026. Data as of December 31, 2025.)

United States Risk Assets Remain the Main Course

Foreign investors are comfortable holding and adding US risk assets while tapering their holdings of US treasuries, some of this warranted by the prospect of a Minsky moment when considering the fiscal situation. Couple this with global markets continuing to find their footing, and it may mean the marginal dollar flowing into foreign markets is not a one-off, but an enduring theme over the next decade. We feel confident that the “Sell America” trade is a mischaracterization of the investing environment we find ourselves in today. US capital markets still offer the most depth, transparency, and shock-absorbing capacity of any market in the world, while corporate governance and investor protections remain central pillars, to say nothing of the

entrepreneurial zeitgeist which has made our home an attractive destination for legal and illegal immigrants alike. Foreign investors are effectively treating US Equities as a quality source of predictable earnings growth, while reducing duration risk in Treasuries. For astute observers, America is still the main course. Risk will always be a part of the equation, and thus caution is always warranted in the investing process, but the truth lies in where investor capital is being allocated.

The views expressed represent the opinions of Breakwater Capital Group as of the date noted and are subject to change. These views are not intended as a forecast, a guarantee of future results, investment recommendation, or an offer to buy or sell any securities. The information provided is of a general nature and should not be construed as investment advice or to provide any investment, tax, financial or legal advice or service to any person. The information contained has been compiled from sources deemed reliable, yet accuracy is not guaranteed. Additional information, including management fees and expenses, is provided on our Form ADV Part 2 available upon request or at the SEC’s Investment Adviser Public Disclosure website,

www.adviserinfo.sec.gov. Past performance is not a guarantee of future results.

Breakwater Team

At Breakwater Capital, we work with families across the United States, providing each client with a personalized experience tailored to their current circumstances, future goals, and timelines.

Financial Literacy Is Not Enough and Why Strategy is the Real Differentiator in Today’s Wealth Shift